Featured

Table of Contents

Browsing Credit Inconsistencies in 2026

The monetary environment in 2026 has actually become significantly complex as automatic reporting systems and AI-driven data collection control the credit market. While these innovations goal for speed, they often lead to clerical mistakes, identity mix-ups, or outdated info appearing on customer files. For citizens in Waterbury Credit Counseling, understanding how to challenge these errors is no longer simply a recommendation-- it is a necessity for maintaining monetary health. Modern consumer laws have tightened up the requirements for credit bureaus, however the burden of starting a disagreement still rests firmly on the individual.

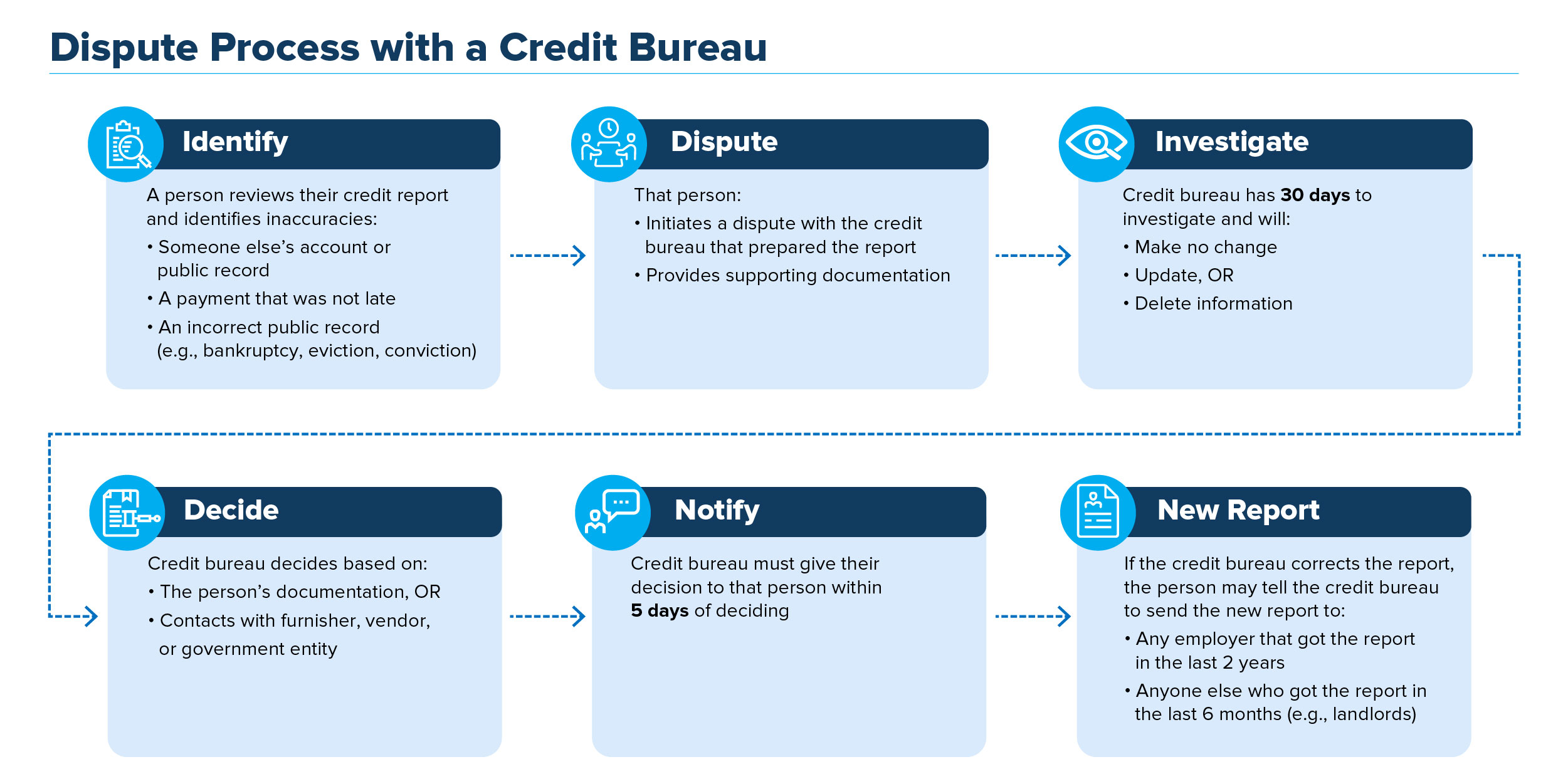

Precision in credit reporting impacts everything from home loan rates to insurance premiums and even employment chances. Keeping high standards for Debt Relief enables consumers to catch errors before they impact loan approvals. When a mistake is recognized, the action needs to be systematic. Under the current 2026 legal requirements, credit bureaus are required to investigate and fix conflicts within a particular 30-day window, supplied the consumer sends adequate evidence to support their claim.

The Rights of Consumers Under 2026 Regulations

Federal policies continue to protect individuals versus the reporting of unreasonable or inaccurate data. Every person in the surrounding region deserves to access their credit report for totally free on a regular basis to make sure that the information held by the significant bureaus is appropriate. These reports work as the structure for an individual's monetary credibility. If a report includes a debt that has actually currently been paid, an account that does not come from the person, or an incorrect payment history, the law offers a clear course for remediation.

Numerous individuals seek assistance from Department of Justice-approved 501(c)(3) not-for-profit credit therapy agencies. These companies supply a buffer in between the consumer and the big financial institutions. Professional Debt Relief Services acts as an essential resource for those facing complex reporting errors. These nonprofits often provide complimentary credit therapy, helping individuals understand which products on their report are really mistakes and which are genuine financial obligations that need a different technique, such as a debt management program.

In 2026, the procedure of contesting an item involves more than simply sending out a letter. It requires a digital or physical proof. This includes copies of bank statements, canceled checks, or court records that show the information on the credit report is incorrect. When a disagreement is submitted, the bureau needs to contact the original lender to validate the information. If the financial institution can not show the financial obligation is accurate within the legal timeframe, the bureau should remove the item from the customer's file right away.

Methods for Effective Credit Keeping Track Of in the United States

Constant tracking is the most efficient way to avoid long-term damage from reporting errors. Waiting up until a loan application is denied is the worst time to discover a mistake. Rather, consumers must use the different tools readily available in 2026 to track modifications to their ratings and report histories in real time. Finding reputable info regarding Debt Relief near Waterbury helps people browse the administration of nationwide credit bureaus.

A thorough evaluation must search for particular red flags:

- Accounts with comparable names or addresses that do not belong to the user.

- Public records, such as tax liens or judgments, that have been settled but still show as active.

- Inaccurate credit limitations that make an individual appear more overextended than they truly are.

- Duplicate accounts that synthetically inflate the total financial obligation load.

If these concerns are discovered, the customer must file disagreements with all three significant bureaus concurrently, as info shared with one bureau is not always immediately upgraded with the others. This ensures consistency throughout the board and avoids a single erroneous report from dragging down an otherwise healthy rating.

Nonprofit Support and Debt Management Programs

For those in the domestic market who are having problem with legitimate financial obligation in addition to reporting errors, specialized programs offer a way forward. Nationwide not-for-profit firms provide financial obligation management programs that combine several regular monthly payments into one lower, manageable payment. These companies work out directly with lenders to reduce rates of interest, making it easier for the consumer to pay off the principal balance. This procedure often assists improve a credit rating with time as the debt-to-income ratio enhances and a history of consistent payments is developed.

Beyond financial obligation management, these 501(c)(3) companies supply HUD-approved real estate counseling. This is especially helpful for homeowners in Waterbury Credit Counseling who are aiming to purchase a home but discover their credit report stands in the way. Therapists deal with people to create a plan that attends to both credit inaccuracies and genuine financial hurdles, ensuring they are prepared for the home mortgage application process. These services are often offered at no expense or for an extremely low fee, reflecting the objective of these firms to support neighborhood monetary literacy.

Legal Defenses and Insolvency Education

In more serious cases, customers might need to check out pre-bankruptcy counseling or pre-discharge debtor education. These are necessary steps in the legal procedure, and they should be completed through a DOJ-approved company. These academic courses are developed to give individuals the tools they need to avoid future financial distress and to handle their credit better after a legal discharge of debt.

Whether dealing with a simple reporting mistake or a complicated financial crisis, the guidelines of 2026 stress transparency. Financial institutions and bureaus are held to high standards of information integrity. When those requirements are not fulfilled, the customer has the power to require a correction. Dealing with a network of independent affiliates and neighborhood groups makes sure that even those in underserved locations have access to the very same level of monetary protection and education as those in significant monetary centers.

The secret to success in any conflict is persistence. It is common for bureaus to at first decline a disagreement, claiming the information was confirmed. In such cases, the consumer must ask for a description of the verification procedure or provide additional, more particular proof. Maintaining a detailed log of all communications with credit bureaus and creditors is a needed part of this effort. With the best documentation and a clear understanding of 2026 customer rights, fixing the record is a workable task that pays dividends in future financial stability.

{kind=link}

Table of Contents

Latest Posts

Utilizing Property Worth to Clear Financial Obligation in Your Region

Optimizing Your Residential Or Commercial Property Worth for Debt Elimination in 2026

How to Construct Wealth Starting With a Better Rating

More

Latest Posts

Utilizing Property Worth to Clear Financial Obligation in Your Region

Optimizing Your Residential Or Commercial Property Worth for Debt Elimination in 2026

How to Construct Wealth Starting With a Better Rating